4 Tips to Secure Your First Mortgage in Aberdeen

If you’re a first-time buyer in Aberdeen looking to buy a home this year, read on for our four top tips to secure your first mortgage.

1. Save deposit

You won’t get anywhere on the property ladder with out money for a deposit.

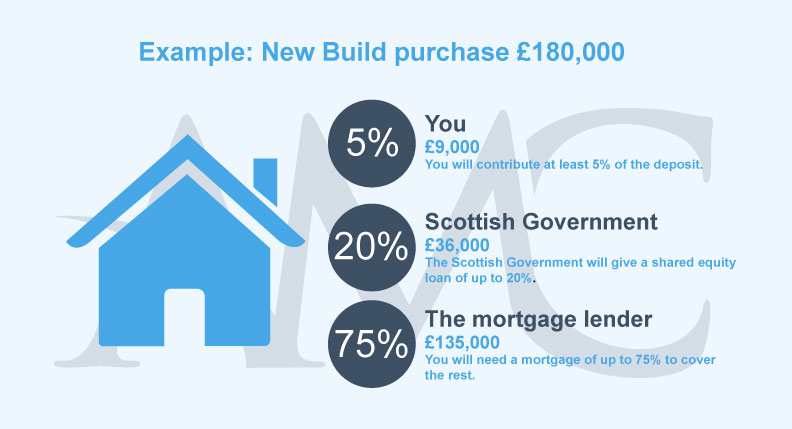

Deposit is key to getting yourself a mortgage. At the moment, you could get a mortgage in Aberdeen with at least 5% of the property’s value. A larger deposit will make you less risky for mortgage lenders and as a result they’ll generally offer you more competitive deals with lower interest rates.

Read our 9 First Time Buyer Deposit Saving Tips.

2. Check credit rating

Having a nice shiny credit rating is a plus.

Even if you have a good income and large deposit, your mortgage application could still be refused if your credit rating is poor. Missing credit card payments or not being on the electoral roll at your current address can make all the difference.

You can check out what your credit rating is by using sites such as Experian, Noddle and ClearScore.

3. Documents Ready

Having the correct documents ready could speed up your first mortgage process. These documents could include:

- Suitable ID

- Last 3 months payslips

- Last 3 months bank statements

4. Speak to someone

By using a mortgage broker in Aberdeen, not only will you receive local knowledge, but a broker will compare hundreds of mortgage lenders and thousands of mortgage deals to see what mortgage suits your circumstances the best.

Aberdeen Mortgage Company are a whole-of-market mortgage broker. We look at mortgage rates from lenders such as Halifax, Nationwide, Barclays and many more to see who has the best deal for you.

Next steps

If you’re looking for some advice of how to get started on the property ladder. Aberdeen Mortgage Company advisers can help explain to you the whole process. We stay with you and hold your hand all the way until you have your key in the door.

View our infographic – 10-step plan to moving into your first home in Aberdeen.

Speak to our expert Aberdeen Mortgage Company advisers to learn how we could help with your first mortgage. You can give us a call on 01224 316200, email us or fill in our online enquiry form.

_ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _

Your home may be repossessed if you do not keep up repayments on your mortgage.

This firm charges a fee of up to £595 for mortgage advice. The fee will depend on your circumstances and will be discussed and agreed with you at the earliest opportunity.

Lifetime Finance Group Limited trading as Aberdeen Mortgage Company is an appointed representative of PRIMIS Mortgage Network, a trading name of First Complete Limited which is authorised and regulated by the Financial Conduct Authority.

You are likely to require a deposit of minimum 5%, your mortgage and deposit must cover a combined minimum 85% of the total purchase price.

You are likely to require a deposit of minimum 5%, your mortgage and deposit must cover a combined minimum 85% of the total purchase price.