With Mother’s Day approaching, we reflect on the importance of mothers in our lives, yet a high percentage of them maybe financially unprotected.

According to a Scottish Widows’ survey of 5,077 adults in the UK, 60% of women with a dependent child have no life insurance.

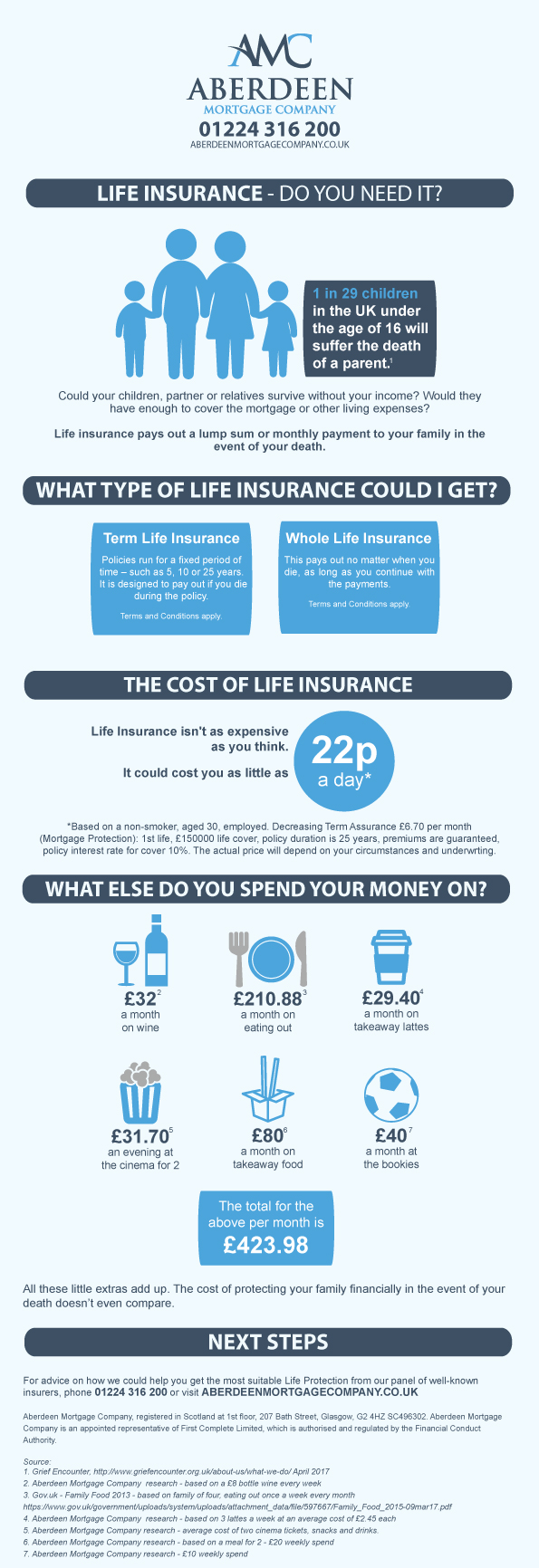

The importance of life insurance

Life insurance comes to the rescue in the event of death. It guards your home and the people in your life by financially protecting them. If you were to die would they have enough to cover the mortgage, bills, general living expenses and funeral costs without you?

1 in 29 children in the UK under the age of 16 will suffer the death of a parent*.

*Source: Grief Encounter, http://www.griefencounter.org.uk/about-us/what-we-do/, February 2018

Life Insurance isn’t as expensive as you think. It could cost you as little as 22p a day**

**Based on a non-smoker, aged 30, employed. Decreasing Term Assurance £6.70 per month (Mortgage Protection) 1st life, £150000 life cover, policy duration is 25 years, premiums are guaranteed, policy interest rate for cover 10%. The actual price will depend on your circumstances and underwriting.

Only 13% of mums have critical illness cover

The Scottish Widows’ survey also reports that a very small percentage of mothers have critical illness cover. Critical illness cover is just as important as life insurance (if not more).

About 31% of mothers admitted their household would be placed at financial risk if they lost their income unexpectedly. 25% claimed they could only pay their mortgage for a maximum of three months. 39% said they would have to use their savings to cover themselves financially if placed in adverse circumstances.

The importance of critical illness cover

Critical illness cover pays out if the worst happens, and you’re diagnosed with a critical illness (specified in your policy) such as cancer or stroke, including children’s critical illness.

Having a Critical Illness Cover in place can help ease your recovery by paying out the money you need for your care and treatment, your recuperation, help pay off your mortgage or make up for lost income.

Speak to one of our expert life insurance advisers about getting the right protection for you. Call 01224 316 200 or request a callback.

Source: Scottish Widows, 2018, http://reference.scottishwidows.co.uk/docs/2018-03-mothers-day-protection.pdf

Please note for these insurance products terms and conditions apply. This information is a summary only. You will receive a full policy document upon application. This policy will set out the terms, conditions and limitations of cover provided under the plan.

Lifetime Finance Group Limited trading as Aberdeen Mortgage Company is an appointed representative of PRIMIS Mortgage Network, a trading name of First Complete Limited, which is authorised and regulated by the Financial Conduct Authority for mortgages, protection insurance and general insurance products. The Financial Conduct Authority does not regulate some forms of Buy to Let. Lifetime Finance Group Limited.